SAGE MOUNTAIN 945 East Paces Ferry Rd NE, Suite 2660, Atlanta, GA 30326

Analysis

Sage Mountain 2022 Outlook

2021 in Review

For “risk-on” financial markets, 2021 continued the strong rebound engineered by policymakers responding to the pandemic’s ill economic effects. Flush consumers, easy money and restored confidence resulted in soaring markets for stocks, real estate, and private companies alike.

We anticipate it will be difficult for the broad markets to repeat this performance. Returns will likely be lower and volatility higher going forward. How the key issues discussed below will turn out is unpredictable, yet we do our best to explain our viewpoint. We believe portfolio diversification, specifically diversification that goes beyond publicly traded stocks and bonds, will be critical to achieving satisfactory results.

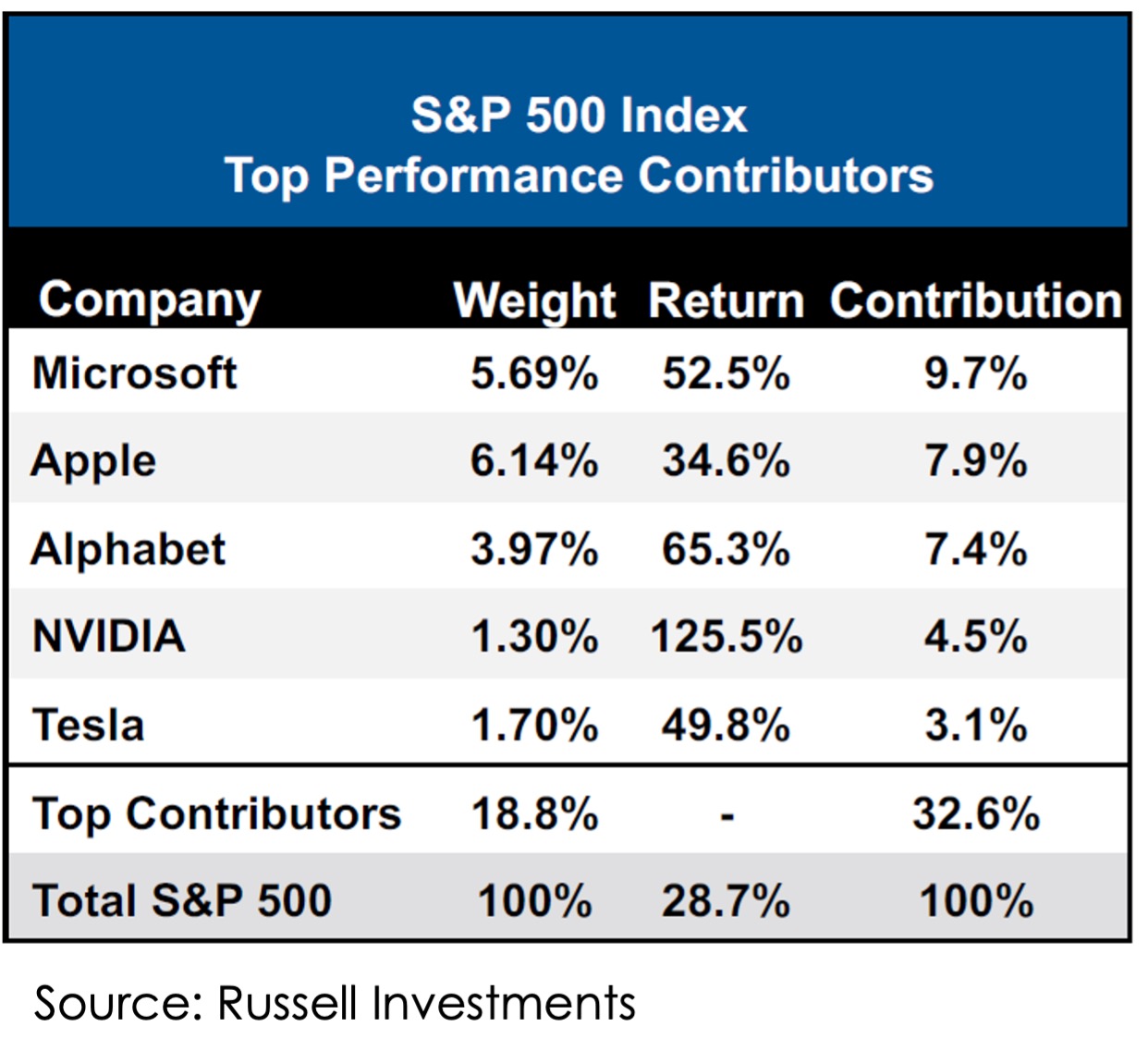

U.S. stocks again performed very well, far outpacing emerging and ex-U.S. developed markets. The U.S. technology sector dominated markets, with the top large cap companies contributing far more than their weight to the index’s return (see below). As economic growth revved higher, however, small cap and mid cap value stocks rose sharply for the first time in years. Inflation began to heat up as limited supply from Covid disruptions met consumers flush with government stimulus, High quality, longer duration bonds suffered as a result.

Inflation has been accelerating since the start of the summer, with the latest CPI reading topping 7%. Shortages of semiconductors have rippled throughout the economy, most notably crimping the production of cars. Oil demand also surprised to the upside. Following significant cutbacks in funding for capital expenditures, the energy market has become much tighter as uncertainty undermines investments that would increase production.

Key Issues

- Covid

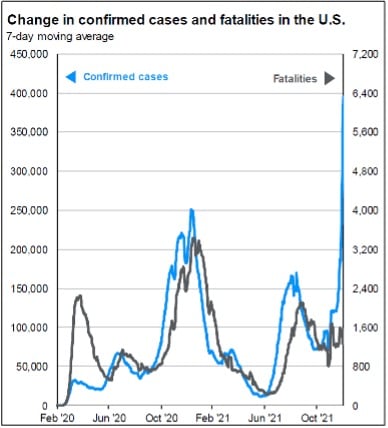

Unfortunately, we are all still talking about Covid-19 and its many variants. The positive news is our ability to cope with the virus and significant progress toward herd immunity mean the economic impacts of 2020 will not be repeated. It may be in fits and starts, but the pandemic is morphing into an endemic disease. The chart at right shows the Omicron variant has resulted in skyrocketing cases – but not in deaths. Unless we see another, deadlier variant, which would cut against the grain of how viruses typically mutate, economic and labor market disruptions should decline from here. Our view: Covid concerns and impacts will decline, creating a more normalized economic environment.

- Inflation and the Fed’s response

Both the economic improvement and higher inflation has prompted the Federal Reserve to accelerate the pace at which it is tapering its bond purchases and project multiple increases in short-term interest rates in 2022. While inflation in components like used vehicles will cool as pent up demand is met and supply chains normalize, housing shortages appear set to continue even with higher interest rates. Combined with upward pressure on wages, inflation will likely run above the Fed’s 2% target in 2022. Current market pricing indicates a 70% chance of three or more rate increases this year. We agree that the Fed will increase rates for the first time in March and likely in June, and further rate hikes will depend on moves in equity markets, longer-term interest rates, and inflation. Our view: investors should continue to limit the duration of their fixed income portfolios and consider investments in private real estate which often performs well in an inflationary environment.

- Equity Valuation

As interest rates fell in recent years, market commentators began to use the acronym, “TINA” (There Is No Alternative), originally popularized by British Prime Minister Margaret Thatcher, to justify ever higher equity market multiples. In reality, the largest components of the U.S. markets have justified their rise with large increases in profitability. In 2021, valuation multiples actually shrank as earnings grew rapidly. By virtually any measure equity valuations remain very high, but underweighting equities based on high valuations has historically been a poor strategy. Consider this: in the last 50 years, 25 of 50 years the market made a new high. After a new high, the market was higher 71% of the time the following year, and 81% of the time after five years. That said, US equity markets have returned over 15% per year since the trough of the Financial Crisis in March 2009, and we do think returns will moderate from here. Our view: we are headed towards slower economic growth, additional wage pressure, higher interest rates, and possibly higher corporate taxes. Investors will need to search creatively for attractive investments given the potential for further earnings growth looks more limited.

- U.S. vs International markets

We plan to stay with our heavily U.S.-tilted stock, bond, and private market weights. We think the earlier and stronger U.S. recovery and higher interest rates will keep the Dollar strong. The biggest engine of international growth has been China and Southeast Asia. This region is facing significant growth headwinds as China attempts to tackle its grossly over-invested real estate sector. This is going to be difficult to pull off and will increase investor uncertainty in an already tainted market. Our view: we will continue to seek out select opportunities abroad, especially in private markets. We continue to see U.S. public markets as more attractive than abroad for U.S. investors.

Asset Class Outlooks

Public Equities

Above, we discussed our preference for U.S. equities vs international. We also discussed the high valuation of the equity market. On the other hand, we believe equities will still produce decent returns, as earnings growth should be positive while a muted rising interest rate cycle keeps a relative value bid under stocks. According to Bloomberg summary of bank strategists, the median year forecast for the S&P 500 is 5,040, an increase of about 7% for the year including dividends. We expect a bumpier ride vs. 2021 as equity market volatility has typically been elevated in midterm election years. Investors with the discipline to remain invested have been rewarded as S&P 500 returns in the year following midterms have averaged 16% since 1944.

Unless we had a very good reason, we would not overweight based on sectors or market capitalization. This year, we think the first half could be better for value strategies as rates rise, inflation runs hot, and GDP growth remains strong. Yet we expect growth and inflation to moderate in the second half, which would be better for growth stocks. Our view: maintain exposure to stocks similar to last year but expect additional volatility as the outlook for growth and inflation is uncertain.

Fixed Income

We continue to believe investors are just not being paid enough to own high quality, low yielding bonds for any reason other than downside protection and portfolio diversification. Until inflation subsides, real rates (interest rates minus inflation) are quite negative. High yield bonds are trading with tight spreads (yields relative to “risk free” Treasury bonds). Compared to the tradeable loan market, which at least has floating interest rates, they are broadly unattractive. In contrast, our analysis points to pockets of opportunity in the structured credit market, most notably in middle market ($50-$75 million in EBITDA), direct lending strategies. Our view: Seek more exposure through loans and asset backed credit versus traditional high yield bonds.

Real Estate

Private Real estate is also generally expensive. However, it has the virtue of rising in value at least in pace with inflation, especially categories with shortages (medical office, industrial real estate, multi-family) and where rents can be reset quickly. The office market is likely to remain very challenging, but all real estate is local, and so significant opportunities exist with skilled managers. Occupied real assets offer stable yields with the potential for cash flow growth during periods of economic growth which we expect. Our view: we plan to focus on U.S. properties benefiting from high user demand: logistics properties (particularly infill logistics assets); suburban multi-family and single-family housing in Sunbelt states. Selectively we will pursue contrarian investment opportunities in stressed corporate and retail opportunities.

Private Equity and Venture Capital:

A reawakened economy and negative real interest rates are contributing to record mergers and acquisitions activity. Announced strategic M&A deal value by US firms totaled $1.1 trillion in 2021, the highest level on record. Meanwhile, the average premium paid to pre-announcement target value rose to 28% in 3Q 2021, above the 5-year average. Institutional money and the search for higher returning assets will keep private equity companies in the market seeking to acquire and grow businesses for resale. In addition, many traditionally “non-tech” businesses can benefit from the software revolution the economy is undergoing, creating new opportunities for PE sponsors to generate returns.

Venture capital has unquestionable been very hot in recent years. However, we expect significant growth in the space to continue, further transforming the business world. Because of money flooding into early-stage investments, we see later-stage companies (and funds focused on them) as relatively more attractive.

Our view: selectively overweight private investments, but we think the large buyout market is less attractive. Focus on growth private equity and late-stage venture capital which are relatively attractive compared to early-stage VC outside of specific sectors. While the most successful early-stage opportunities may offer higher return potential, late-stage VC and growth equity returns are a safer bet with fewer losers, which we think is better at this point in the cycle.

Private Credit:

On the supply side, borrowers continue to look to the private markets due to their relatively greater speed and certainty of execution, after many were burned by public markets and banks pulling back capital during more uncertain times. Equally, borrowers value the adaptability and partnership of private lenders, who remain hungry for deals. On the demand side, the global search for yield continues but today also includes a demand for assets that can hedge inflation and protect capital. Our view: we expect an active market that is more attractive than traditional bonds, and in many cases worth the required illiquidity to participate.

Infrastructure and Transport:

Infrastructure investing is becoming ever more important, providing opportunities for lower volatility returns that historically have low correlation to equities and bonds. We believe core infrastructure assets, especially in OECD markets, will continue to find investor support. However, the influx of ESG capital has made finding returns in some sectors, such as power generation, more difficult.

We expect backlogs in global supply chains, shipping delays, and port congestion to continue to lift profits in the transport sector – for example shipping and rails. Ongoing growth in e-commerce and strong consumer demand in major economies should continue to support investor sentiment. Even after pandemic-related supply chain constraints ease, a tight supply of transportation assets may endure. Our view: as the pandemic recedes, we hope to make investments in critical infrastructure such as airports, toll roads, and shipping assets, but are taking significant caution given the macroeconomic sensitivity and the need for a reliable partner in such investments.

![]()

In Conclusion:

The team at Sage Mountain remains highly engaged with our clients across all aspects of investing, financial planning, and trust and estate planning. The coming year should be more normal, but the road to get there could well be rocky as extraordinary fiscal and monetary measures unwind and political uncertainty increases. We hope the above outlook proves useful to communicate how we view the current opportunity set. Please reach out to your Wealth Advisor to discuss any of these topics.

Thank you again for your trust as a partner.

Russ Allen

Director of Investment Strategy

Sage Mountain

Tony Cox

President & Chief Investment Officer

Sage MountainPast performance is not indicative of future results. Please see the disclosures below.

This information is for one-on-one presentation only and is in response to a specific request. This information should not be distributed to any other parties. Forecasts. estimates and certain information herein are based upon proprietary research and should not be interpreted as financial advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. It should not be assumed that any of the recommendations or characteristics discussed herein will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable. It is not possible to invest directly in an index. The portfolio characteristics and recommendations shown here are based on only the information that has been provided to us This analysis could change significantly as we learn more about your account and suitability The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account: (ii) investment restrictions applicable to the account. if current investment strategies and techniques based on changing market ‘ dynamics or client needs. SMA is an investment adviser registered with the U.S. Securities and and (iii) market exigencies at the time of investment. SMA reserves the right to modify its Exchange Commission. Registration does not imply any particular level of skill or training. More information about the advisor including its investment strategies and objectives can be obtained by visiting www.sagemountainadvisors.com. All references to performance are gross of fees unless otherwise noted. Gross of fee performance does not reflect the deduction of investment advisory fees. The portfolio’s return will be reduced by advisory fees and other expenses that may be incurred in the management of the portfolio. Returns presented gross of management fees include the reinvestment of all interest and other earnings. As an example, the effect of investment management fees on the total value of a client’s portfolio assuming (a) quarterly fee assessment in arrears, (b) $50,000,000 initial investment, (c) portfolio return of 3%6 a year, and (d) 0.25% annual investment advisory fee would be $127.215 in the first year, and cumulative effects of $671,937 over five years and $1,441,217 over ten years. Actual management fees may vary, depending upon, among other things, the applicable management fee schedule and portfolio size. A complete description of SMA’s fee schedule can be found in Part 2 of its FORM-ADV which is available at www.sagemountainadvisors.com or by calling (404) 795-8361.

SMA-21-000704