SAGE MOUNTAIN 945 East Paces Ferry Rd NE, Suite 2660, Atlanta, GA 30326

Analysis

What to Consider When Rebalancing a Portfolio: Riding Performance or Staying on Target?

December 29. 2021

Research from William Bernstein suggests that “rebalancing works best with volatile, uncorrelated assets whose returns are roughly similar,” and “taxability may completely eliminate any rebalancing benefit at all.”

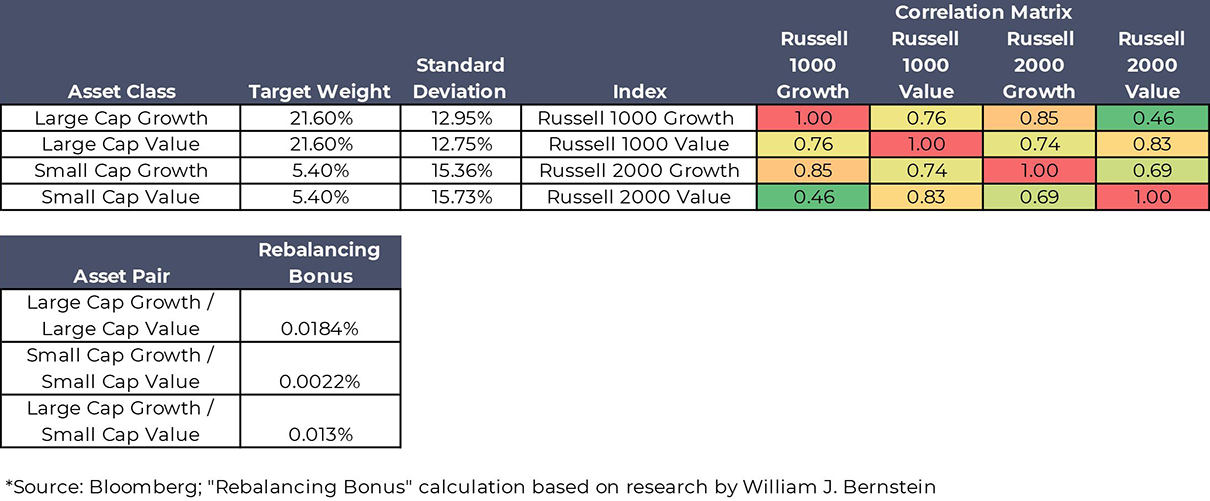

In a previous post, he calculates a “rebalancing bonus” based on the weights of assets in a portfolio, their variance, and their covariance2 . To attempt to calculate the benefit from rebalancing across asset pairs in your portfolio, we applied his formula to different asset classes using the target weights and data from Bloomberg. This focuses on sub asset classes within US equity. Correlations between fixed income and equity are lower and between US and international equities they are lower in some circumstances, so the benefit to rebalancing across those asset classes is clearer.

On a more granular level, however, this data shows that rebalancing across US equities is expected to produce a small benefit. We paired large cap growth and value which have the largest weights in the portfolio, small cap growth and value, and large cap growth and large small cap value which have the lowest correlation amongst the US equity sub asset classes.

The above calculations do not factor in the negative tax impacts of rebalancing which could further reduce the expected benefit.

Further research from Berstein’ and AQR4 indicates that the potential from rebalancing depends on the assumption that cross-asset returns will revert to their historical means. That has, by definition, been the case historically, but there is no guarantee that will continue. As many disclaimers will tell you, past performance is not indicative of future results. And while history is often a useful guide, at least in theory tectonic shifts in the economic environment like the persistence of low interest rates and the heightened importance of monetary policy may alter the balance of returns between growth vs. value and US vs. international equities.

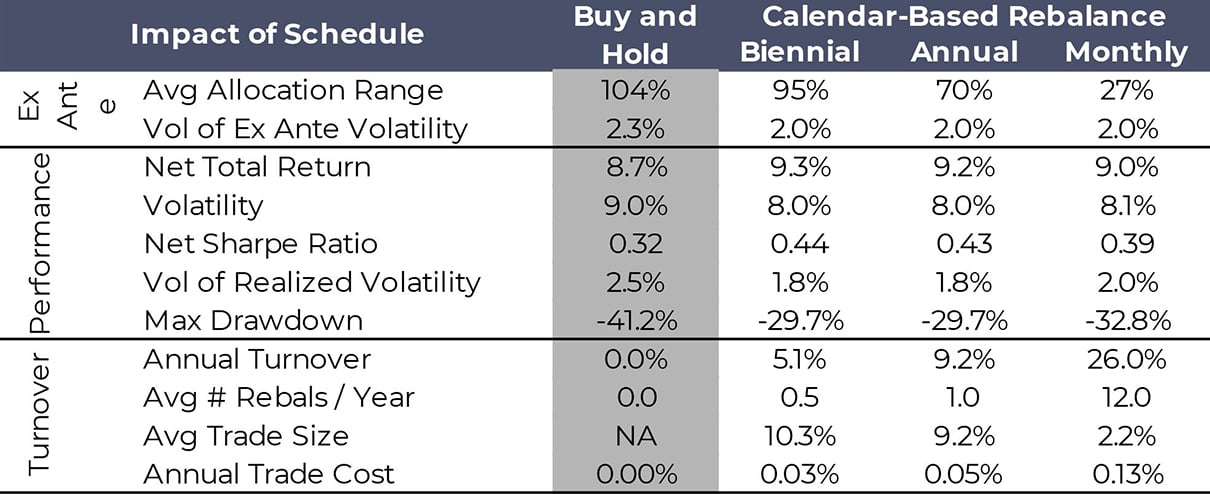

The paper from AQR also proposes that momentum effects are an important consideration when considering the appropriate rebalancing strategy. We agree there is considerable evidence for momentum effects which indicates that rebalancing over short time frames (i.e. less than once per year) is suboptimal. Based on their research, the difference in risk and returns from different calendar and trigger-based rebalancing strategies is minimal, but biennial rebalancing produces the highest Sharpe Ratio and return and lowest maximum drawdown of all the methods included in their analysis:

So why ever rebalance? With a pure buy and hold strategy, asset classes with higher returns will become an increasingly larger portion of the portfolio over time. Because of that, while over long time periods there are minimal or even negative expected returns from rebalancing, it does enable portfolios to stay closer to their risk targets.